For property owners, maximizing the potential of their real estate investments is paramount. Whether you’re a seasoned investor or new to the game, understanding the financial landscape of your property is critical to making informed decisions and optimizing returns. That’s where financial underwriting comes into play, as well as income calculators and Excel spreadsheets as a calculation tool. They emerge as an indispensable tool in your arsenal. In this article, we’ll delve into why these resources are essential for property owners and how they empower you to unlock the total value of your assets.

Income calculators offer property owners invaluable insights into the income potential of their properties, enabling them to make strategic decisions that align with their financial objectives. By accurately estimating rental income and factoring in expenses, owners can gauge the profitability of their investments and identify growth opportunities. This financial clarity empowers owners to proactively manage their properties, adjust rental rates, and optimize occupancy levels to maximize revenue streams. Additionally, these calculators facilitate comparative analysis, allowing owners to benchmark their properties against similar assets in the marketplace and identify areas for improvement. By leveraging these tools alongside Excel spreadsheets for more in-depth analysis, owners can fine-tune their investment strategies, identify potential risks, and capitalize on emerging opportunities.

In conclusion, financial underwriting through income calculators is a game-changer for property owners looking to extract maximum value from their investments. By comprehensively understanding their properties’ income potential and market positioning, owners can make informed decisions that drive long-term success and profitability. With these tools at their disposal, owners can navigate the complexities of real estate investment with confidence and precision, ultimately realizing their vision for their properties and securing a prosperous future.

If you would like more information or have any questions, please post a comment below or contact us. We also offer a service to help buyers underwrite assets; learn more here.

In real estate, a property listing is not just a mere snapshot. It’s a strategic canvas where every detail matters. One crucial brushstroke often sets successful listings apart is the spotlight on income potential and current occupancy rates. It’s a statement of fact, strategically positioning your property to captivate the eyes of potential buyers and investors. To look at it better, Occupancy or vacancy rates as an inverse, refer to the percentage of rental units occupied at any given time. High occupancy rates translate to higher rental income. In this case, it can instill confidence among the buyers and investors as it demonstrates market demand, effective management, and the property’s appeal to tenants, which is good for seeing the factual income potential of a property.

Displaying current occupancy rates provides a real-time snapshot of the property’s desirability and tenant satisfaction. It’s not just about saying it’s occupied; it’s about conveying the property’s demand, stability, and attractiveness as a lucrative investment. On the other hand, Income potential is the enchanting waltz that allures potential buyers since your property is a potential revenue stream. By articulating its income-generating possibilities, whether through rental income, commercial spaces, or other avenues, you present a compelling narrative that transcends the physical aspects of the property.

For expert investors, the income potential and occupancy rates are not just details but decision-making factors. Placing this information in your listing creates a magnetic pull for those seeking property and a good investment opportunity.

In conclusion, the art of real estate listings goes beyond the basics. It’s essential in positioning your property in the market. By highlighting income potential and occupancy rates, you’re not just presenting data. It instills a sense of assurance in your potential buyers that will help them see your financial sensibilities and investment goals. This will attract the right attention and pave the way for a successful transaction.

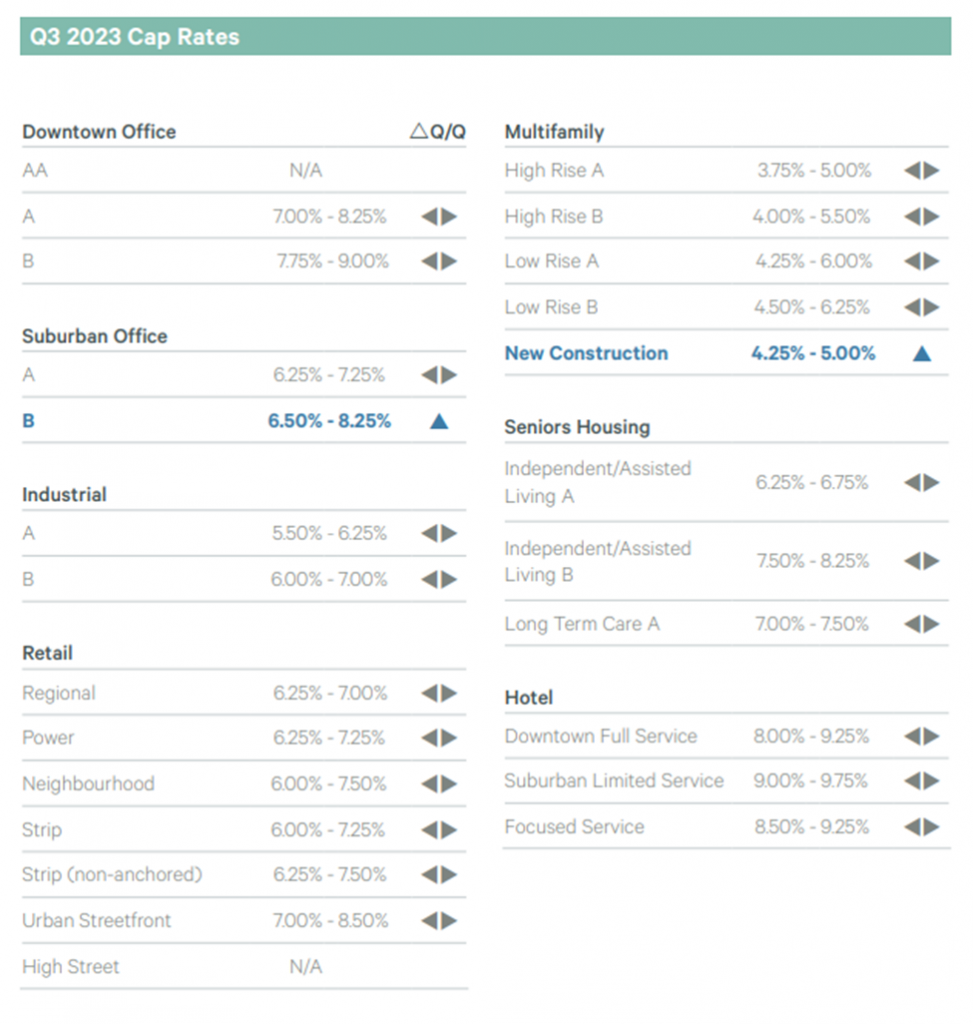

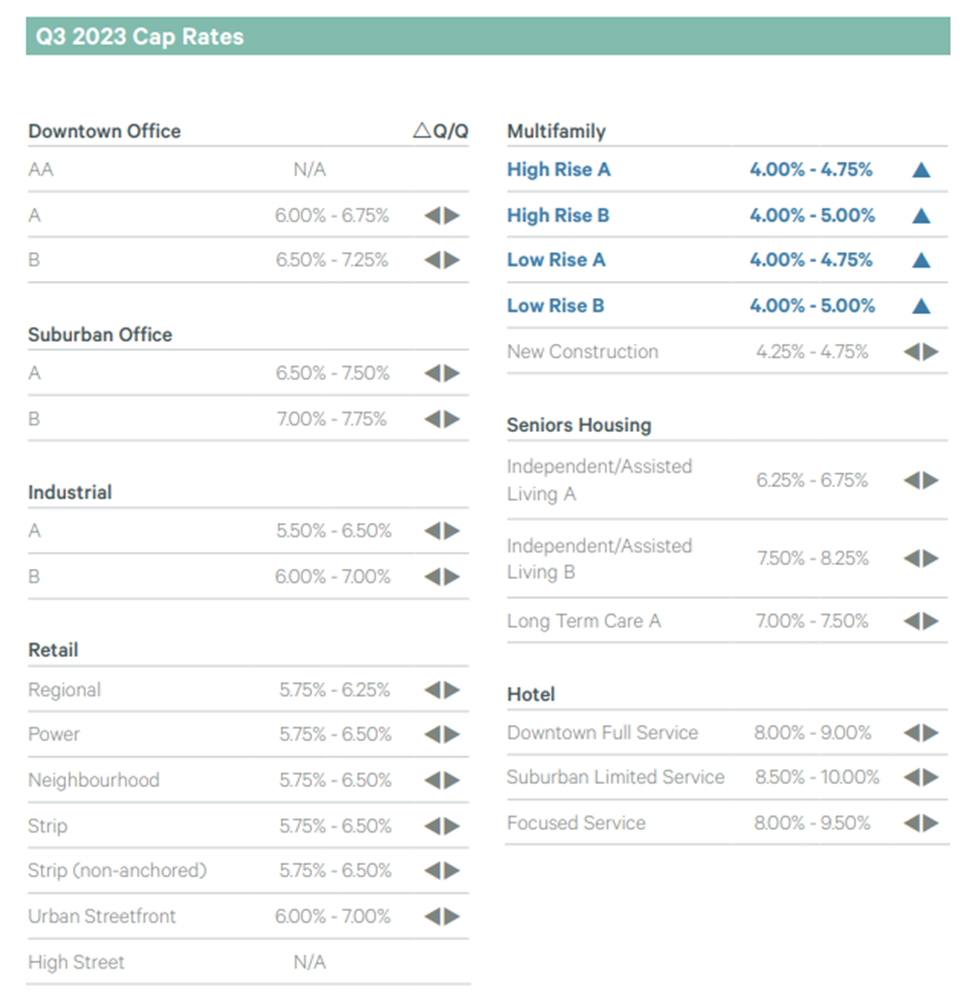

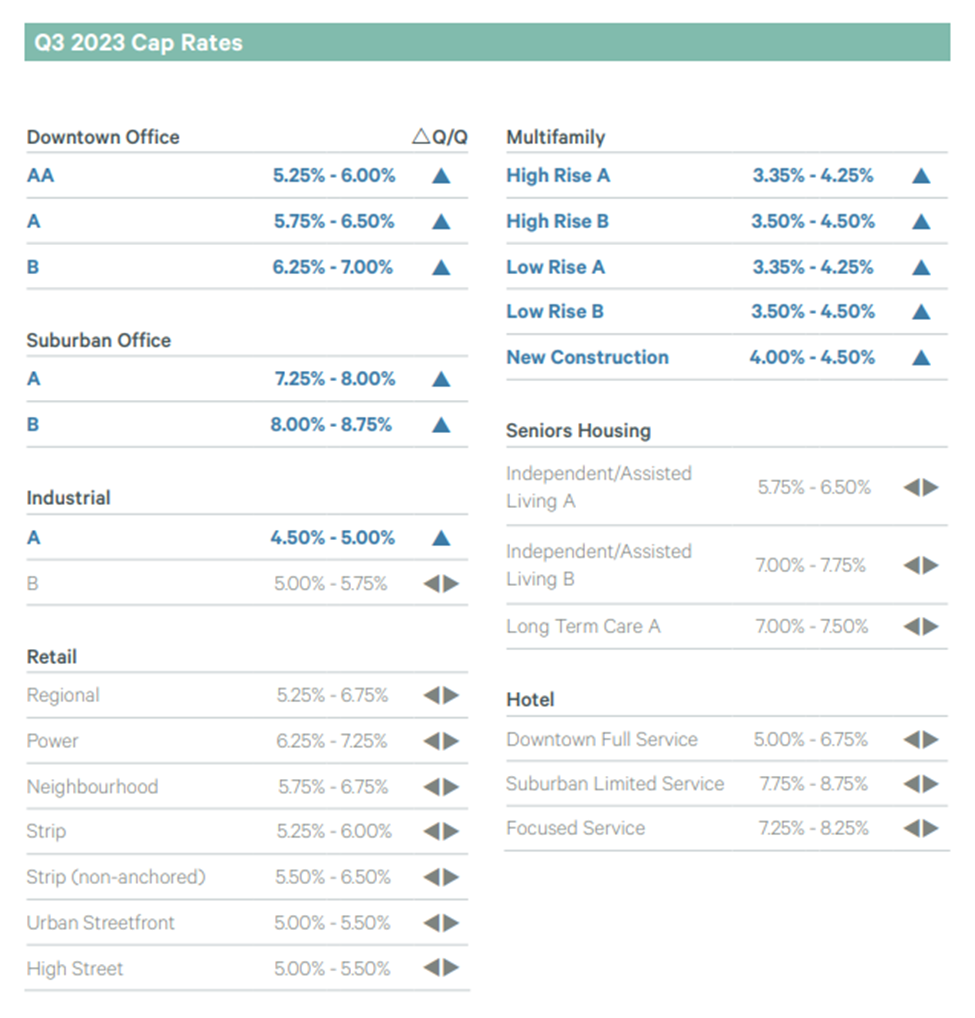

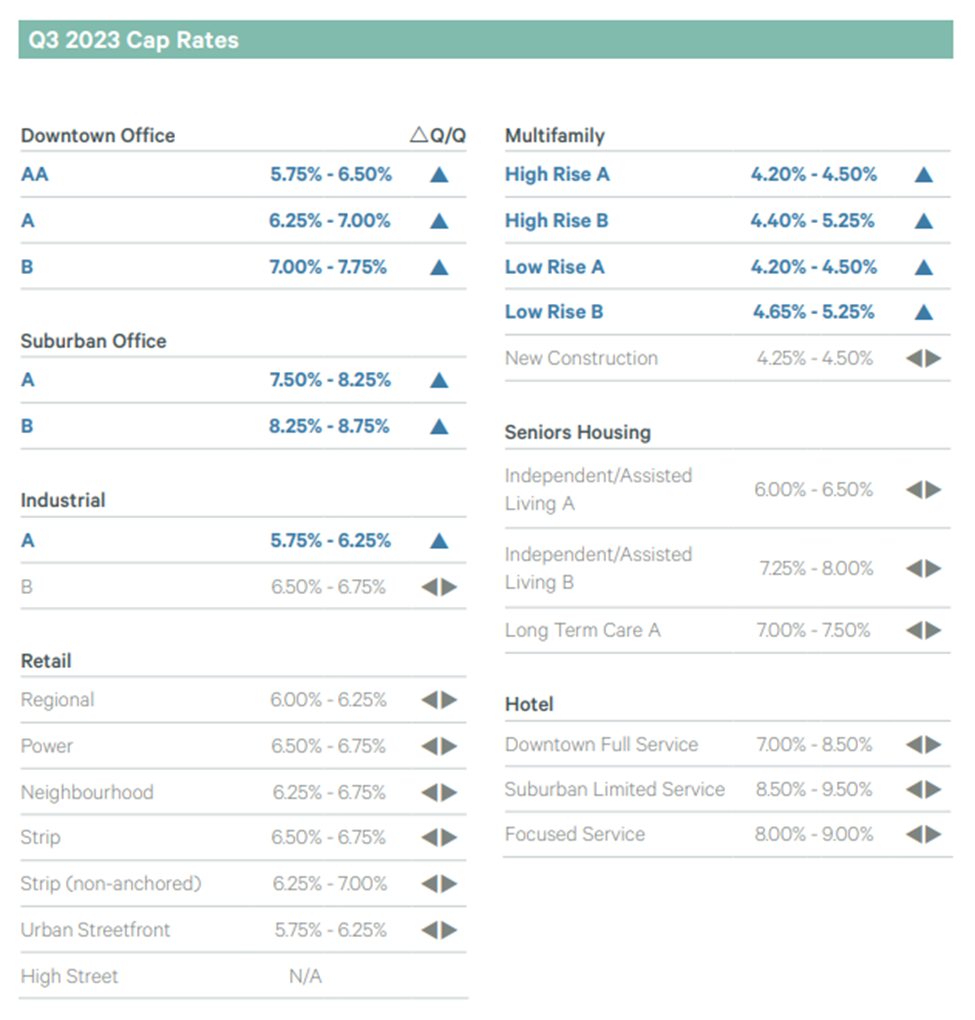

According to the CBRE’s Q3 2023 Canadian Cap Rate Report, Ontario’s multifamily sector has decompressed slightly, with the national average High Rise and Low Rise categories increasing 12 bps quarter-over-quarter to 4.55%.

This growth indicates a robust market. This trend suggests increased demand for multifamily properties, potentially leading to rising property values and providing opportunities for property owners. The accelerated growth may attract developers, fostering new projects and expanding the multifamily housing market.

Following are some important multi-family graphs worth checking:

National Multifamily Investment Trends

The report notes that Ontario’s strong economy and population growth continue to make it a desirable location for multifamily investment.

London, ON Investment Trends

Kitchener-Waterloo Investment Trends

Toronto, ON Investment Trends

Ottawa Investment Trends

In conclusion, this positive trajectory points towards Ontario’s flourishing multifamily housing market. The province’s robust economy and continuous population growth contribute significantly to its appeal to investors. This could translate into an opportunity for real estate investors to enter the market at lower prices and an opportune time to maximize returns.

When it comes to real estate investment in Canada, there’s a financial concept you need to grasp, and it is called “Capital Expenditures,” often referred to as “CapEx.” Think of CapEx as the expenses you’ll encounter to keep your property in good shape and improve its value over time. Understanding CapEx is vital. In this blog, we will break down Capital Expenditures, what they cover, and how to calculate them. By the end, you’ll know how to make better financial decisions, protect your investments, and ensure your real estate portfolio thrives for the long haul.

Capital Expenditures, often referred to as “CapEx,” represent the financial investments allocated to obtain, upgrade, or maintain a property, including equipment acquisition. These expenditures are categorized as CapEx if they involve new purchases or serve to extend the property’s lifespan, such as repairing the roof, installing a furnace, or repainting the building. Accurate assessment and consideration of both current and future CapEx are critical when determining a property’s value. Property owners must also incorporate CapEx into their rent calculations. Failing to account for or miscalculate CapEx could result in setting rent rates too low, leading to financial losses and negative cash flows for property owners.

Here are some of the most common capital expenditures in real estate:

New HVAC equipment

Major appliances

A complete overhaul of the plumbing

A complete overhaul of the electrical work

Bathroom remodels

Kitchen remodels

New roofs

New windows

New flooring

Balcony repairs

Siding

Paving or repaving a parking lot

Waterproofing of building or envelope

Additions to the property

Minor repairs and maintenance are typically not classified as capital expenses. For instance, replacing an entire roof is a capital expense, whereas repairing a small roof section falls into regular operating costs. The new roof prolongs the property’s lifespan, while minor repairs merely maintain its current usefulness. Similarly, purchasing a new furnace is a capital expense, while replacing furnace components is standard repair work. Upgrading an electrical panel is likely a capital expense, but replacing a light fixture is not.

Calculating Capital Expenditures is very easy. As an investor, it’s your responsibility to estimate the replacement timeline for major items. To create a capital expenditure budget, list these big-ticket items and their expected lifespans. Additionally, assess the status of each item in its useful life. This comprehensive list helps you plan for each expenditure. Once you’ve identified each expenditure, you can now use this simple formula to get the Capital Expenditure.

Let me give you a better example; for instance, a new roof costs approximately $50,000 and typically lasts 20 years. To calculate the annual CapEx, divide $50,000 (total replacement cost) by 20 years (expected lifespan) to get $2500 per year for roof-related expenditures. Apply this method to all significant maintenance items to estimate your yearly spending. If needed, break these expenses into monthly budgets for greater convenience.

Since this money isn’t being spent yearly, it sits in a reserve account and can be invested in vehicles such as GIC, where your capital is protected and income guaranteed. This way, you can also use compounding interest to minimize your cash outlay and maximize your IRR for every dollar within the investment.

In conclusion, Capital expenditures are among the largest, yet necessary expenses tied to investment properties. It’s true; you must invest money to reap rewards, and CapEx is no different. You can’t avoid them, so it’s wise to budget for them. Successfully managing a real estate business means not only accounting for these expenses but also budgeting for them wisely.

Unlocking the doors to multifamily property ownership is a significant financial milestone, but it often comes with a complex web of financial requirements. Among these, the down payment is a crucial piece of the puzzle. Whether you’re a seasoned real estate investor or a newcomer to the multifamily market, understanding the intricacies of down payment requirements is paramount. In this guide, we will delve into the world of underwriting multifamily properties, shedding light on the factors that influence down payment demands and offering expert insights to help you navigate this critical aspect of property investment.

Investing in multifamily real estate comes with distinct requirements depending on the type of mortgage, commercial or residential, available for your rental property. The rules differ whether you’re eyeing a property with five units or more or one with precisely four units. Before choosing what type of rental property you will invest in, you need to know the basic qualities to qualify for a rental property mortgage. Here are a few things that you need to consider:

You must have a credit score, ideally above 680

Proof of earnings whether you’re employed, run a business or earn commissions.

Low debt profile, indicating that you have sufficient extra money to cover your mortgage payments.

Proof that you have sufficient funds to cover the rental property’s down payment and closing costs. Some lenders may also require you to have a reserve fund for expenses as well.

If you recall, choosing the type of rental property dictates different requirements. A property may be classified as residential or commercial based on local zoning by-laws. A simple way to tell if a residential rental property requires a residential or commercial mortgage is by reviewing the number of units in the property. Commercial rental properties are buildings with six or more units, while properties with one to five units (depending on the lender) are categorized as residential. In underwriting a rental property, mortgage terms for commercial properties can be more challenging than those for residential rental properties. This post won’t dive into the complexities of commercial property mortgages; instead, we’ll concentrate on understanding the down payment requirements for residential rental properties. The primary factors that dictate your down payment amount for such properties are the property’s price and the number of units it contains. So, how much do you usually need to put down for residential rental properties? Typically, it falls within the range of 5% to 35%.

To be eligible for a down payment of less than 20%, you must have 1-4 units and be within a residential zoning, the purchase price for the building cannot exceed $1 million, and It must be owner-occupied (you must live in one of the units for at least 1 year).

For owner-occupied rental buildings with 1-4 units, minimum down payment requirements are as follows:

Owner-occupied with 1-2 units, the down payment is 5%.

Owner-occupied with 3-4 units, the down payment is 10%.

For investment properties, with six or more units or properties worth more than $1,000,000, a commercial mortgage with a minimum down payment of 20% is required. If you apply for a CMHC loan for such a property, you may find that CMHC has appraised your property for less than your purchase price, forcing some buyers to make larger down payments of up to 35% of the purchase price. Governmental programs are available for affordable housing projects that can help reduce downpayment for such properties to 5% while offering amortization of 40 to 50 years.

In conclusion, understanding the nuances of down payment requirements is crucial for successful multifamily property investments. As you embark on your real estate journey, the knowledge gained from this guide will empower you to make informed decisions, ensuring that your investment endeavours are financially sound and strategically advantageous.

If you would like more information about multi-family real estate investing or have any questions, please make sure to post a comment below or contact us.

In the ever-changing realm of real estate investing, grasping the influence of interest rates is vital, particularly for multi-family properties. With solid demand in the multifamily market amid economic uncertainty, it’s crucial to comprehend the short-term and long-term consequences of interest rate hikes. Let’s first explore the concept of inflation to get a clearer picture of how an interest rate hike affects the multifamily market. Inflation is the gradual increase in the overall price level of goods and services within an economy over time. It erodes the purchasing power of money, leading to increased expenses for investors and developers. The Bank of Canada employs interest rates as a tool to manage inflation. When interest rates go up, the BoC’s goal is to reduce consumer spending and borrowing, thereby slowing economic growth, and curbing inflationary pressures. These rates can influence the overall profitability, financing options, and investment strategies for multifamily properties.

Negative Impact of rising interest rates on the multifamily investment landscape

Costly Debt Dynamics

When interest rates rise, debt becomes pricier, influencing investor returns and property prices. This shift in market dynamics might lead to decreased transaction volume or investors opting to hold onto properties, awaiting a more favorable seller’s market.

Variable-Rate Debt Dilemma

Investors with variable-rate debt may face challenges during resets. A property generating positive cash flow at 3% interest may not be sustainable at 6%. This could lead to negative cash flow, potentially resulting in loan defaults and foreclosures as operational reserves run dry or loan covenants are breached.

Job Market Jitters

Rising interest rates often correlate with job layoffs. According to a recent PwC survey, half of industry executives are reducing headcount or planning to, with 52% implementing hiring freezes. In the multifamily market, anticipating slower growth, investors and property managers might trim staff in response to operational challenges. While a short-term fix, job losses can trigger late payments and collection costs, further impacting property profitability.

However, while high-interest rates are generally perceived as a challenge in the realm of investments, there are scenarios where they can bring about positive impacts in multifamily real estate:

Enhanced Returns for Lenders

Higher interest rates mean that lenders, such as banks or financial institutions, earn more from the interest charged on loans. This can make lending to multifamily property investors more attractive, potentially leading to increased loan availability.

Stability in Market Conditions

High-interest rates can contribute to a more stable real estate market. When interest rates are high, property values may be less prone to rapid and unpredictable fluctuations. This stability can be beneficial for long-term investors looking for predictability in their investment returns.

Reduced Speculative Activity

High-interest rates may discourage speculative investment behavior, where investors buy properties with the sole intent of selling them quickly for a profit. This reduction in speculative activity can contribute to a more sustainable and balanced market, preventing the formation of property bubbles that can lead to market crashes.

Discourages Overleveraging

High-interest rates act as a natural deterrent against excessive borrowing or overleveraging. This can be positive for the overall health of the multifamily investment sector, as it encourages investors to use a more cautious approach in financing their acquisitions, reducing the risk of financial instability.

Attractive Yields for Fixed-Income Investors

High-interest rates make real estate investments more appealing to fixed-income investors seeking stable and attractive yields. Multifamily properties, known for their reliable cash flow, become a more attractive option compared to other investment vehicles in a high-interest-rate environment.

Potential for Bargain Purchases

High-interest-rate environments may lead to a decline in property prices as demand softens. For investors with sufficient capital and a long-term perspective, this presents an opportunity to acquire properties at more favorable prices, with the potential for significant appreciation when interest rates eventually decrease.

In conclusion, high interest rates in multifamily investments can have some silver linings. They might bring stability to the market, making property values less jumpy. Also, they discourage risky behaviors like buying and selling properties quickly, making the market more reliable. High rates could mean fewer people taking big loans, preventing financial troubles down the road. For those looking to invest for the long haul, high rates might mean a chance to buy properties at lower prices. Remember, while high rates pose challenges, they can also create opportunities for savvy investors willing to navigate the market wisely.

If you’re interested in finding out more about investing in Multi-family properties, please make sure to leave a comment or contact us

Investing in real estate can be a rewarding venture, but it comes with its own jargon that can confuse beginners. One such term you’ll often encounter is “Cap Rate.” But what exactly is the Cap Rate, and why is it crucial for investors? Let’s break it down in simple terms.

A Cap Rate is short for Capitalization Rate, a fundamental metric used in real estate to evaluate a property’s potential return on investment. In simpler terms, it’s a way to measure the profitability of a real estate investment.

Cap Rate is a percentage that indicates the potential return on an investment. A higher Cap Rate generally suggests a higher potential return but may also come with higher risk. Conversely, a lower Cap Rate may indicate a safer investment with lower returns.

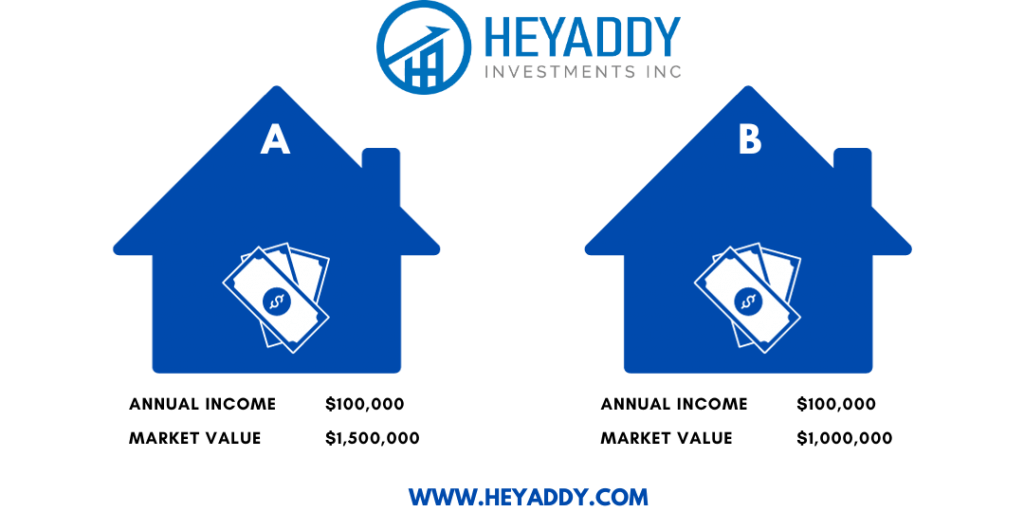

Cap rate is calculated using a straightforward formula, it is equal to Net Operating Income (NOI) divided by the current market value of the asset. (see the photo below for the graphic illustration)

A situational example:

Addy is an investor looking to buy an investment property. From taking real estate courses, he remembers that the capitalization rate is an effective metric in evaluating real estate properties. Addy identifies and compares two properties with their annual income and market values:

After calculating the properties’ cap rates, Addy realizes that Property B has the highest cap rate of 10%.

Addy may base his purchase on the rate alone in a straightforward scenario. However, it is just one of many metrics that can be used to assess the return on commercial real estate property. While it provides a good estimate of a property’s potential return, it’s not the only metric to consider. In fact, various other metrics like the gross rent multiplier, internal rate of return, debt coverage ratio and many more should also be considered. So, when assessing a real estate opportunity, it’s wise to consider a combination of these metrics, not just the Cap Rate, to get a more comprehensive picture of its attractiveness.

Terminologies explained:

Net Operating Income (NOI): This is the total income generated by a property minus the operating expenses. It includes rental income but excludes mortgage payments and income taxes.

Current Market Value or Acquisition Cost: This represents the property’s current value or the cost at which it was acquired.

While Cap Rate provides a quick snapshot of a property’s potential return, it does have limitations. It doesn’t consider financing costs, future capital expenditures, or changes in property value over time. Investors should use the Cap Rate alongside other metrics for a comprehensive analysis.

In conclusion, Cap Rate is a valuable tool for real estate investors, offering a quick assessment of a property’s potential return on investment. However, it’s crucial to consider it in conjunction with other factors to make well-informed investment decisions. Whether you’re a seasoned investor or a novice exploring real estate, understanding Cap Rate is a key step in navigating the world of property investment.

We’ve been working diligently on couple of projects including a large project with 70+ units. Please make sure to check out the projects we have listed on our website below