Low Cap Rates and Rent Control in Ontario

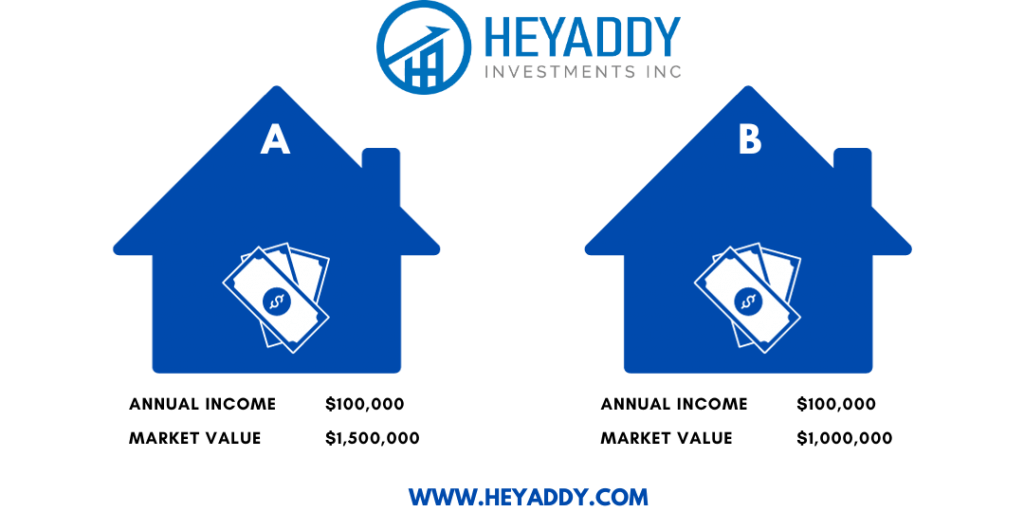

When it comes to real estate investments in Ontario, one of the key metrics that investors often consider is the capitalization rate, commonly referred to as the cap rate. This metric is crucial in evaluating the potential return on investment for a particular property. A low cap rate can be a topic of concern for investors, as it implies a different risk-return profile for the investment. In the context of Ontario real estate, low cap rates generally indicate that the property’s income is insufficient in relation to its market value. In other words, it implies that the property is priced high compared to the income it generates. This can be attributed to several factors, such as high demand for real estate, low supply, and low interest rates, which push property values up and subsequently reduce the cap rates.

Ontario has rent control in the form of the Residential Tenancies Act, and it also impacts market cap rates for properties. These rules affect both landlords and tenants and have a substantial impact on the rental market. Rent control is a government policy that regulates how much a landlord can increase the rent for a residential property. The primary goal of rent control is to protect tenants from unreasonable rent hikes, ensuring that housing remains affordable and preventing widespread displacement due to excessive rental increases.

In Ontario, rent control is governed by the Residential Tenancies Act. Under these rules, rent control applies to most private rental units, including apartments, single and semi-detached houses, and units in residential complexes. However, not all rental properties are subject to rent control. For instance:

New Rental Units

Newly built units or rental properties that underwent significant renovations on or after November 15, 2018, are not subject to rent control.

Social and Affordable Housing

Rent control does not apply to housing units that receive government subsidies or are part of affordable housing programs.

Landlords in Ontario are subject to rent control regulations. This means they can’t always charge the current market rent if it’s rising faster than what the government allows for rent increases. In such cases, the legal rent they can charge might be lower than what the property could actually fetch in the market. This unutilized potential rent remains untapped until the tenant moves out, which can affect the property’s cap rate negatively/lower. Property sellers can use this lower rent as leverage to justify a lower cap rate, showcasing the gap between the current rent and the market rate. In a seller’s market, where property inventory is limited, buyers might be willing to accept a slightly lower cap rate to secure a property with untapped income potential. This dynamic highlights the importance of understanding the local rental market and its impact on property valuation in Ontario.

In the dynamic world of Ontario real estate, being aware of factors like capitalization rates and rent control is essential for both investors and tenants. Low cap rates can raise concerns, signalling property pricing is out of sync with income generation due to various market forces. On the other hand, rent control regulations are a vital aspect of maintaining affordable housing for tenants and ensuring that rent increases are fair and regulated. Whether you’re an investor looking for the right opportunity or a tenant seeking protection, understanding these elements is crucial for a balanced and informed approach to the Ontario real estate landscape. It’s all about finding the equilibrium where investors can thrive, and tenants can access affordable housing. So, whether you’re crunching the numbers as a property owner or looking for a rental home, these factors play a significant role in shaping the Ontario real estate experience.

If you would like more information about multi-family real estate investing or have any questions, please make sure to post a comment below or contact us.